Does the Fed Control Mortgage Rates? What Changes and What Doesn't

The Fed sets the federal funds rate, which moves credit cards, HELOCs, and savings yields. The 30-year fixed mortgage follows the 10-year Treasury. Here is the mechanical difference.

Written with AI assistance; every figure is checked against our calculators and primary sources, and reviewed by Ethan Ginsberg before publishing.

The bottom line

A 0.25-percentage-point change in the 30-year fixed rate moves the payment on a $320,000 loan by about $54 a month.

No. The Federal Reserve sets only the federal funds target range, which moves short-term, variable rates: credit card annual percentage rates (APRs), home equity lines of credit (HELOCs), and savings and certificate of deposit (CD) yields. The 30-year fixed mortgage tracks the 10-year Treasury yield and mortgage-backed securities, not the Fed. The FOMC's next decision posts June 17, 2026, and fixed rates often move before it.

What does the Fed actually set?

The FOMC, the Fed's rate-setting committee, votes on a target range for the federal funds rate. That is the interest rate banks charge each other for overnight loans. The range is typically a 0.25-percentage-point band (for example, "4.25% to 4.50%"), and the exact level is published in the statement released after each meeting at federalreserve.gov. The June 17, 2026 statement is the next scheduled release.

That single number is the Fed's main lever. It is not a mortgage rate, a savings rate, or a credit card rate. It is a wholesale rate between banks. Everything else sits downstream, and some things are far more downstream than others.

What moves directly when the Fed acts?

Short-term and variable rates hug the federal funds rate. The clearest link is the prime rate, the rate banks use as a baseline for many consumer loans. By long-standing convention, the prime rate sits 3 percentage points above the top of the federal funds target range. The Federal Reserve's H.15 release (federalreserve.gov/releases/h15) publishes the prime rate, and it has moved in lockstep with the funds rate's upper bound for decades.

Because these products are priced off prime or other short-term benchmarks, they tend to reprice within a billing cycle or two of a Fed move:

| Product | Typical benchmark | Reprices |

|---|---|---|

| Credit card APR | Prime rate + margin | Next statement cycle |

| HELOC | Prime rate + margin | Next statement cycle |

| Adjustable-rate mortgage (after reset) | Index + margin | At scheduled reset |

| Savings / money market | Loosely tied to funds rate | Days to weeks |

| New CDs | Bank pricing off short rates | Days to weeks |

The Consumer Financial Protection Bureau (consumerfinance.gov) describes how variable-rate credit cards and HELOCs are tied to the prime rate, which is why a Fed change shows up on those statements quickly.

Why doesn't the 30-year fixed mortgage follow the Fed?

The 30-year fixed rate is a long-term rate, and long-term rates are set by the bond market, not by the FOMC. Lenders bundle mortgages into mortgage-backed securities (MBS) and sell them to investors. Those investors compare MBS yields to the 10-year Treasury yield, the return on a 10-year U.S. government bond. So the 30-year mortgage rate moves with the 10-year Treasury plus a spread for risk and prepayment.

The data shows the relationship. The Federal Reserve Economic Data service tracks the 10-year Treasury yield (fred.stlouisfed.org, series DGS10) and Freddie Mac's Primary Mortgage Market Survey 30-year rate (fred.stlouisfed.org, series MORTGAGE30US). The two lines rise and fall together, with the mortgage rate riding above the Treasury yield by a roughly 1.5-to-3-point spread.

There is a twist. Because the 10-year yield reflects what bond traders already expect the Fed to do, the mortgage rate often moves before a Fed meeting and sometimes against the decision. If the market has priced in a cut weeks ahead, the mortgage rate may already reflect it by the time the FOMC announces. A Fed move that matches expectations can leave the 10-year yield, and mortgage rates, barely changed.

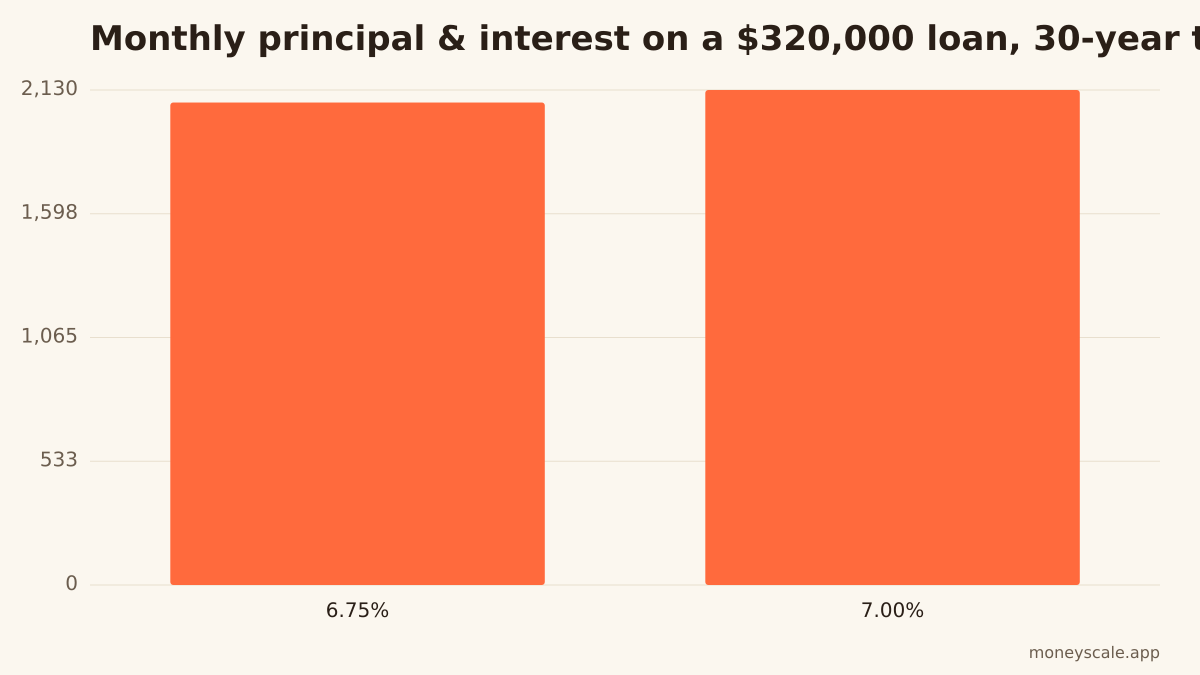

How much does a quarter point change a mortgage payment?

Fixed mortgage rates move in their own market, but the math of a rate change is the same regardless of cause. Take a $400,000 home with 20% down, leaving a $320,000 loan on a 30-year term.

At a 6.75% rate, the monthly principal and interest comes to about $2,076. At 7.00%, it rises to about $2,130. That 0.25-percentage-point difference is about $54 a month, or roughly $648 a year, on the same loan balance. Run other balances and rates in the companion tool at /tools/mortgage-payment.

Will mortgage rates drop after the June 17 meeting?

That is a forecast, and the mechanics above are why the Fed decision alone cannot answer it. The 30-year fixed rate will follow the 10-year Treasury yield and MBS demand, which respond to inflation data, growth data, and what the bond market had already priced in before June 17, 2026. A Fed cut, hold, or hike tells you what happened to the overnight bank rate. It does not, by itself, tell you where the 10-year Treasury closed that day.

What the Fed decision reliably changes is the short, variable side of a household balance sheet: card APRs, HELOC rates, and the yields on savings and new CDs. The 30-year fixed mortgage lives in a different market.

The short version

- The Fed sets the federal funds target range; the statement posts June 17, 2026.

- Prime rate = funds rate upper bound + 3 points, which directly drives card and HELOC rates.

- The 30-year fixed mortgage tracks the 10-year Treasury yield and MBS, and often moves before or against a Fed decision.

- On a $320,000 loan, a 0.25-point rate change is about $54 a month.

Run your numbers

Plug your own figures into the Mortgage Payment calculator and see your specific outcome.

Open Mortgage PaymentSources

Related reads

400k Mortgage Monthly Payment at 7%: Full Cost

The 400k mortgage monthly payment at 7% on a 30-year fixed: $2,129 principal and interest, about $2,646 all-in with taxes and insurance.

Read itPMI Explained: What Private Mortgage Insurance Costs and When It Cancels

Private mortgage insurance protects your lender, not you — and you pay for it when you put down less than 20%. Here's what it costs, the federal law that forces it to cancel, and how to get it off your statement as early as possible.

Read itHow the Fed's Rate Decision Hits Your Credit Card APR

The prime rate is the lever that connects an FOMC move to your variable-rate card. Here's the formula, the lag, and the math on a $6,000 balance.

Read itWhat Is the Fed Dot Plot? How to Read the SEP

A plain-English guide to the Fed's dot plot and the Summary of Economic Projections, with the June 17, 2026 release time and how to read the median dot.

Read it

Money Scale Weekly

Read another one like this on Thursday?

We send one short, sourced money read per week. Tied to mortgage payment and the other Money Scale pillars. Free, no spam, one click to unsubscribe.

Drop your email and you're in. We send one short read on Thursday — and nothing else without your asking.