How the Fed's Rate Decision Hits Your Credit Card APR

The prime rate is the lever that connects an FOMC move to your variable-rate card. Here's the formula, the lag, and the math on a $6,000 balance.

Written with AI assistance; every figure is checked against our calculators and primary sources, and reviewed by Ethan Ginsberg before publishing.

The bottom line

The U.S. prime rate equals the top of the federal funds target range plus 3 percentage points, and most credit cards charge that prime rate plus a fixed margin.

The Fed's June 17, 2026 decision doesn't touch your card directly. It moves the federal funds target range, which sets the U.S. prime rate, defined as the top of that range plus 3 percentage points. Most cards charge prime plus a fixed margin, so a 0.25-point change reaches your statement within one to two billing cycles.

How does a Fed move reach your credit card?

The Federal Open Market Committee (FOMC) sets a target range for the federal funds rate, the rate banks charge each other for overnight loans. The FOMC does not set credit card rates. The link runs through one number in the middle: the prime rate.

The prime rate is the rate commercial banks publish for their most creditworthy customers. By convention, the U.S. prime rate sits at the top of the federal funds target range plus 3 percentage points. The Wall Street Journal publishes the benchmark based on rates posted by large banks, and the Federal Reserve reports the same prime rate daily in its H.15 Selected Interest Rates release. When the FOMC raises or lowers the target range, banks reset prime by the same amount, usually that day or the next business day.

Most variable-rate credit cards are priced as prime + a fixed margin. The margin is set in your contract based on the product and your credit profile, and it does not move when the Fed moves. So if your card is "prime + 17.99%" and prime drops 0.25 points, your APR drops 0.25 points too.

What is the prime rate right now?

Going into the June 17, 2026 meeting, the federal funds target range stood at 3.50% to 3.75% (set in December 2025 and held at the April 28–29, 2026 meeting), putting the prime rate at 6.75% (3.75% upper bound + 3.00%), per the Federal Reserve's H.15 release and the FOMC's published target-rate history. If the Committee changes the range by 0.25 points, prime moves to either 6.50% or 7.00%. If the range is left unchanged, prime stays at 6.75%.

| Component | Level going into June 17, 2026 |

|---|---|

| Federal funds target range (upper bound) | 3.75% |

| Add-on by convention | +3.00 points |

| U.S. prime rate (H.15) | 6.75% |

The Fed's H.15 release is the primary record for the prime figure, and the St. Louis Fed's FRED database tracks the same Bank Prime Loan Rate series over time.

What's the difference between a variable and a fixed APR?

The Consumer Financial Protection Bureau (CFPB) explains the difference in plain terms. A variable APR is tied to an index, almost always the prime rate, and changes when the index changes. A fixed APR does not move with an index, though issuers can still change it with advance written notice under federal rules.

On the disclosure box of a cardholder agreement, a variable rate reads as the index plus the margin, for example "15.24% to 25.24%, based on the Prime Rate." That sentence is the tell: if the word "variable" or "Prime Rate" appears, your rate resets when the Fed moves. APR stands for annual percentage rate, the yearly cost of borrowing stated as a percentage. Most card issuers charge interest using a daily periodic rate, dividing the APR by 365 and applying it to the average daily balance, with interest compounding daily.

How fast does the APR actually change?

There's a built-in lag. Card agreements specify a date for reading the index, often the prime rate in effect on the last or first day of a billing cycle. A Fed change today moves prime almost immediately, but your statement rate updates only on the first day of the billing cycle that begins after the new prime takes hold. In practice that lands within one to two billing cycles. A Fed move never changes the margin; only the prime portion shifts.

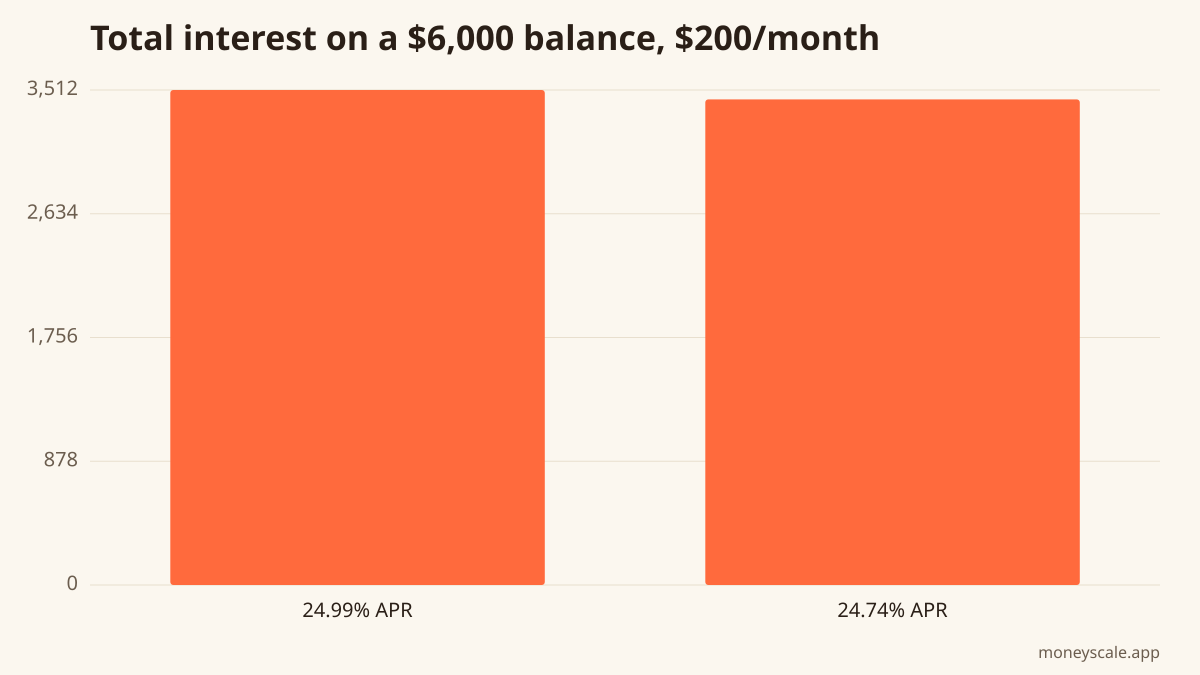

What does a 0.25-point change do to a $6,000 balance?

Here's the mechanics on a real number. Take a $6,000 balance with a $200 fixed monthly payment, and compare a 24.99% APR against a 24.74% APR, a 0.25-point difference.

At 24.99%, the balance takes 48 months to clear and costs about $3,512 in interest. At 24.74%, it still takes 48 months but costs about $3,445. The gap is roughly $67 over the life of the payoff, and the payoff month doesn't move.

The math points to one conclusion: a single 0.25-point Fed step is small on a typical revolving balance. The size of the payment matters far more than a quarter point. The credit card payoff calculator can show months-to-payoff and total interest for any combination of balance, APR, and payment.

Where do the numbers come from?

The federal funds target range and prime rate come from the Federal Reserve's H.15 release and the FOMC's target-rate history. The variable-versus-fixed APR mechanics come from the CFPB. The interest figures above use a standard fixed-payment amortization at the stated APRs.

Run your numbers

Plug your own figures into the Credit Card Payoff calculator and see your specific outcome.

Open Credit Card PayoffSources

Related reads

What the Fed's Rate Decision Means for Your Money

A mechanical guide to how the federal funds rate reaches your credit cards, HELOC, mortgage, and savings—pegged to the June 16–17, 2026 FOMC meeting.

Read itHow to Pay Off Credit Card Debt: The 4-Step Plan That Works on $5K or $50K

A plain-English, four-step plan to pay off credit card debt — stop the bleeding, pick a payoff order, cut the interest rate, and automate it. Works the same whether you owe $5,000 or $50,000.

Read itDoes the Fed Control Mortgage Rates? What Changes and What Doesn't

The Fed sets the federal funds rate, which moves credit cards, HELOCs, and savings yields. The 30-year fixed mortgage follows the 10-year Treasury. Here is the mechanical difference.

Read itWhat Is the Fed Dot Plot? How to Read the SEP

A plain-English guide to the Fed's dot plot and the Summary of Economic Projections, with the June 17, 2026 release time and how to read the median dot.

Read it

Money Scale Weekly

Read another one like this on Thursday?

We send one short, sourced money read per week. Tied to credit card payoff and the other Money Scale pillars. Free, no spam, one click to unsubscribe.

Drop your email and you're in. We send one short read on Thursday — and nothing else without your asking.