How Money Market Fund Yields Work After the June 2026 Fed Meeting

A plain-English look at what a money market fund is, how its yield tracks the federal funds rate, and why those yields stayed near current levels after the Fed held rates on June 17, 2026.

Written with AI assistance; every figure is checked against our calculators and primary sources, and reviewed by Ethan Ginsberg before publishing.

The bottom line

On June 17, 2026 the FOMC held its target range steady, and its updated dot plot showed roughly half of members projecting at least one 2026 rate change.

A money market fund (MMF) is an SEC-registered mutual fund that holds short-term debt like Treasury bills and repurchase agreements, so its yield tracks short-term interest rates. Those rates sit close to the federal funds rate. On June 17, 2026 the Federal Reserve held its target range steady, so MMF yields stayed near current levels instead of dropping.

What happened at the June 2026 Fed meeting?

The Federal Open Market Committee (FOMC), the Fed body that sets the federal funds rate, kept its target range unchanged at its June 17, 2026 meeting, according to the Fed's press release (federalreserve.gov, monetary20260617a.htm). The federal funds rate is the rate banks charge each other for overnight loans, and it anchors most other short-term rates in the economy.

Alongside the decision, the Fed published its quarterly Summary of Economic Projections (SEP), which includes the "dot plot." That chart shows where each FOMC participant expects the policy rate to land at year-end. In the June 2026 SEP, the projections rose from the prior round, with roughly half of participants penciling in at least one rate change before the end of 2026 (federalreserve.gov, June 2026 SEP).

The takeaway for cash yields is simple: a hold is not a cut. When the Fed leaves its target range in place, the short-term instruments inside money market funds keep paying close to what they paid the week before.

What is a money market fund, exactly?

A money market fund is a mutual fund registered with the Securities and Exchange Commission (SEC) and governed by Rule 2a-7. That rule limits the fund to high-quality, short-maturity debt. Typical holdings include:

- Treasury bills — short-term IOUs issued by the U.S. Treasury

- Repurchase agreements ("repo") — very short-term collateralized loans

- Short-term government agency debt and, in some funds, high-grade commercial paper

Because every holding matures quickly, the fund constantly reinvests at whatever short-term rate exists right now. That is why an MMF yield moves with the federal funds rate within weeks rather than years. The SEC describes these funds and their structure on Investor.gov.

One term appears on every fund page: the 7-day SEC yield. This standardized number, defined by the SEC, annualizes the fund's net income over the most recent seven days after subtracting fund expenses. It lets you compare two funds on the same basis. You can find it on the fund provider's site and in the fund's prospectus.

Why did MMF yields stay high after the hold?

A money market fund's yield is essentially a pass-through of the short-term rates its holdings earn, and those rates are pinned near the federal funds target range. The chain works like this:

| Fed action | Effect on short-term debt rates | Effect on MMF 7-day yield |

|---|---|---|

| Cuts the target range | Move down within weeks | Drifts down |

| Holds the target range | Stay near current level | Stays near current level |

| Raises the target range | Move up within weeks | Drifts up |

The June 17, 2026 decision was a hold, so the middle row applies: short-term rates stayed roughly where they were, and MMF yields followed. The dot plot projects where participants think rates may go. It does not change today's rate, so it does not move current yields by itself.

How is an MMF different from a bank savings account or CD?

This distinction trips up many readers. A money market fund is an investment product, not a bank deposit. The SEC is explicit that money market funds are not FDIC-insured (Investor.gov). The Federal Deposit Insurance Corporation (FDIC) insures bank deposits — checking, savings, money market deposit accounts, and certificates of deposit (CDs) — up to $250,000 per depositor, per insured bank, per ownership category (fdic.gov).

Watch the wording, because two similar names mean different things:

| Feature | Money market fund (MMF) | Money market deposit account (MMDA) |

|---|---|---|

| What it is | SEC-registered mutual fund | Bank deposit account |

| Regulator/rule | SEC, Rule 2a-7 | Bank, FDIC-insured |

| FDIC insurance | No | Yes, up to limits |

| Yield quoted as | 7-day SEC yield | APY |

A CD is also a bank deposit: money is locked in for a set term at a fixed annual percentage yield (APY), the rate that includes compounding. Because the terms differ, the way to compare earnings differs too.

How do you compare what cash earns?

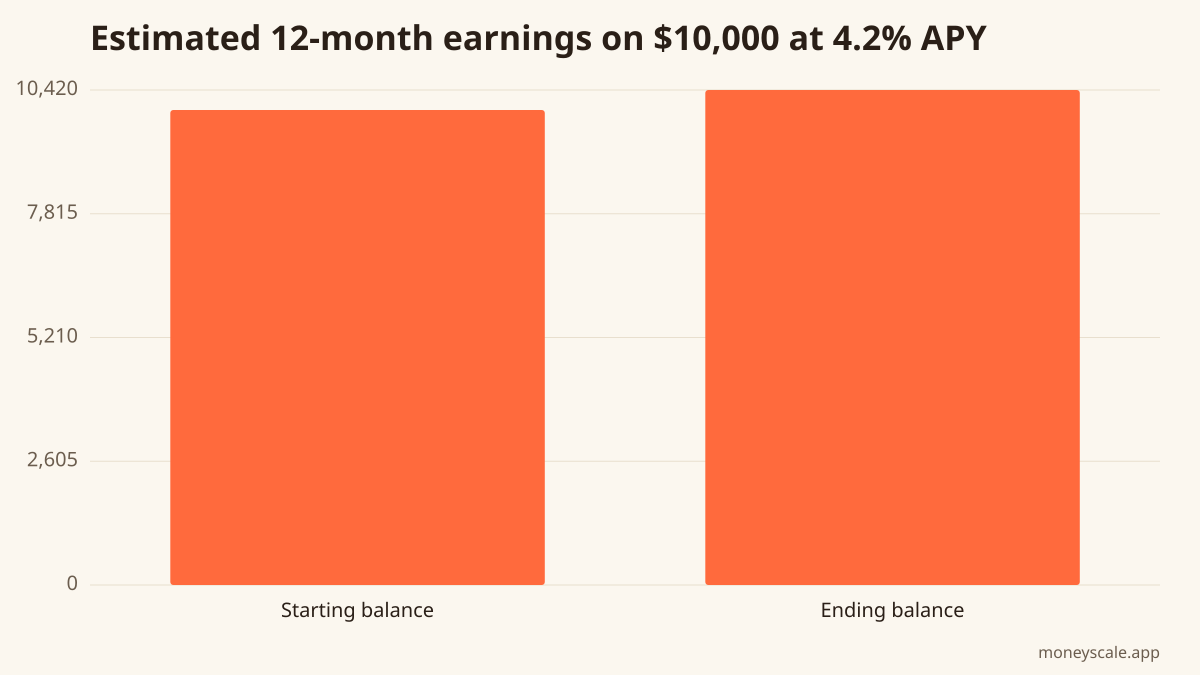

The cleanest comparison runs the same dollar amount through each rate for the same period. Take a $10,000 balance at a 4.2% APY held for 12 months: it would grow to about $10,420, or roughly $420 in interest. You can run your own figures with the CD calculator at /tools/cd to see estimated earnings at a given rate and term.

Keep one difference in mind. A CD's APY is fixed for the term. An MMF's 7-day yield floats and can rise or fall as the underlying short-term rates change, which is exactly why a Fed hold keeps it near current levels rather than locking it there.

The bottom line on the mechanics

A money market fund holds short-term debt, so its yield tracks short-term rates set off the federal funds rate. The Fed held that rate on June 17, 2026, which is why MMF yields did not fall after the meeting. The dot plot is a set of projections, not a rate change. And unlike a savings account or CD, a money market fund carries no FDIC insurance, a fact the SEC states plainly.

Sources

Related reads

What Is the Fed Dot Plot? How to Read the SEP

A plain-English guide to the Fed's dot plot and the Summary of Economic Projections, with the June 17, 2026 release time and how to read the median dot.

Read itQ2 Estimated Taxes Are Due June 15, 2026: How Quarterly Payments Work

The second-quarter 2026 federal estimated tax payment is due June 15. Here is how quarterly payments work, who owes them, the safe-harbor rule, and how self-employment tax is figured — with the real numbers.

Read itHow a CD Ladder Works (and When Each Rung Matures)

A plain-English walkthrough of CD ladders: staggered maturities, APYs, early-withdrawal penalties, FDIC limits, and the year-by-year math.

Read itHow the Fed's Rate Decision Hits Your Credit Card APR

The prime rate is the lever that connects an FOMC move to your variable-rate card. Here's the formula, the lag, and the math on a $6,000 balance.

Read it

Money Scale Weekly

Read another one like this on Thursday?

We send one short, sourced money read per week. Tied to cd and the other Money Scale pillars. Free, no spam, one click to unsubscribe.

Drop your email and you're in. We send one short read on Thursday — and nothing else without your asking.