Refinance Break-Even Point: Is Refinancing Worth It?

The simple math that tells you whether a mortgage refinance pays for itself, with a June 2026 rate example.

Written with AI assistance; every figure is checked against our calculators and primary sources, and reviewed by Ethan Ginsberg before publishing.

The bottom line

Refinancing a $320,000 loan from 7% to 6% saves about $210 a month, so $9,600 in closing costs takes roughly 46 months to recover.

Refinancing pays off only if you keep the new loan past its break-even point: total closing costs divided by your monthly payment savings. Drop a $320,000 loan from 7% to 6% and the payment falls about $210 a month. Against $9,600 in closing costs, that is roughly 46 months, or about 3.8 years, to break even.

What is a refinance break-even point?

A refinance replaces your current mortgage with a new one. You pay closing costs up front (or fold them into the balance), and in exchange you get a lower rate, a different term, or cash out of your equity. The break-even point is the month where the money saved finally equals what the refinance cost. The formula is plain:

Break-even months = total closing costs ÷ monthly payment savings

Before that month, the loan is behind. After it, every payment at the lower rate is real savings. Sell the house, move, or refinance again before break-even and the deal cost money. The Federal Reserve's consumer guide to mortgage refinancings frames the same break-even idea.

How much does a refinance cost?

Closing costs on a refinance typically run 3% to 6% of the loan amount, per Freddie Mac. On a $320,000 loan, that range is $9,600 to $19,200. The CFPB's guidance on mortgage closing costs lists the usual line items: loan origination or application fees, an appraisal, title search and title insurance, recording fees, and sometimes discount points (an optional up-front fee that buys down the rate).

The lender must itemize these on a Loan Estimate within three business days of the application, and again on a Closing Disclosure before signing. Those two CFPB-mandated forms hold the real "total closing costs" number for the formula above.

How does the break-even math work at June 2026 rates?

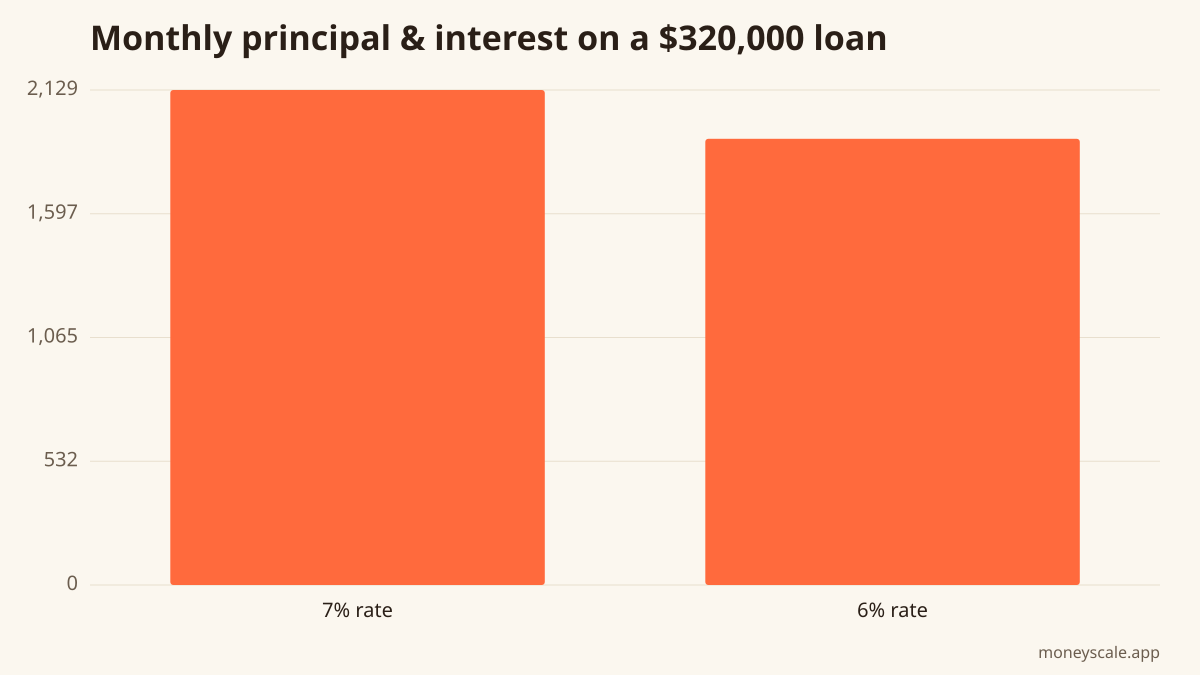

Say you owe $320,000 on a 30-year loan at 7% and refinance into a new 30-year loan at 6%.

| Item | At 7% | At 6% |

|---|---|---|

| Loan balance | $320,000 | $320,000 |

| Monthly principal & interest | $2,129 | $1,919 |

| Monthly savings | — | $210 |

The gap is about $210 a month. With $9,600 in closing costs (3% of the loan), the math is $9,600 ÷ $210 ≈ 46 months. Stay in the loan longer than that and the savings turn positive; leave sooner and they don't.

Run your own figures — actual closing costs and actual payment savings — in the refinance break-even calculator.

Where do you find today's average rate?

The benchmark most homeowners watch is Freddie Mac's Primary Mortgage Market Survey (PMMS), which reports the average 30-year and 15-year fixed rates and is released every Thursday. The same series is mirrored on the Federal Reserve's FRED database as "30-Year Fixed Rate Mortgage Average" (series MORTGAGE30US), which shows the full history.

A national average is a reference point, not a quote. An offered rate depends on credit, loan size, equity, and points paid, so the only rate that matters for the formula is the one on your own Loan Estimate.

Does rolling costs into the loan change the math?

Closing costs can be paid in cash at closing or added to the new balance. Both paths run through the break-even formula, but they shift the inputs.

- Pay cash: the loan amount stays lower, so monthly savings are larger and break-even comes sooner. The trade-off is cash up front.

- Roll costs into the loan: no cash out of pocket, but the larger balance trims the monthly savings and pushes break-even out. Interest also accrues on those costs for the life of the loan.

Neither is automatically better; they trade up-front cash for a longer payback. The calculator handles either version once the correct loan amount and savings go in.

Rate-and-term vs. cash-out: what's the difference?

Two refinance types behave differently:

- Rate-and-term refinance: changes the interest rate, the loan term, or both, without taking extra cash. The break-even formula fits this version cleanly.

- Cash-out refinance: replaces the loan with a larger one and hands over the difference in cash. Because the balance grows, the payment can rise even when the rate falls, so simple break-even math falls short — part of the new payment buys cash, not just a lower rate.

Why doesn't a lower rate alone guarantee savings?

Resetting the clock matters. Refinance 8 years into a 30-year loan into a fresh 30-year loan and the remaining balance stretches back over a full 30 years. The monthly payment can drop while total interest over the life of the loan rises, because interest accrues for more years. A lower rate trims the monthly number; a longer term adds years of payments. Comparing both the monthly payment and the total interest — figures spelled out on the Loan Estimate — shows the whole trade.

What do the latest June 2026 readings show?

The Mortgage Bankers Association's Weekly Applications Survey, an industry tracker of mortgage application volume, reported in its release for the week ending June 12, 2026 that total mortgage application volume decreased 3.8%. On the rate side, Freddie Mac's June 18 PMMS put the average 30-year fixed rate at 6.47%, down from 6.52% the prior week. When rates dip, applications can climb because more existing loans clear their own break-even math. That is a data trend, not a forecast. Where rates go next is unknown, and the only test that settles whether a refi works for a given loan is the break-even calculation on that loan's real numbers.

Run your numbers

Plug your own figures into the Refinance Break-even calculator and see your specific outcome.

Open Refinance Break-evenSources

Related reads

Compound Interest, In Plain English: The Math Behind Your Future Self's Net Worth

Compound interest is the closest thing personal finance has to a cheat code. Here's the formula, the chart that makes it click, and the three numbers that matter more than picking the perfect fund.

Read itHow Money Market Fund Yields Work After the June 2026 Fed Meeting

A plain-English look at what a money market fund is, how its yield tracks the federal funds rate, and why those yields stayed near current levels after the Fed held rates on June 17, 2026.

Read itMid-Year 2026 Paycheck Checkup: Is Your Tax Withholding on Track?

How federal withholding works, why June is the natural time to check it, and how to use the free IRS Tax Withholding Estimator for 2026.

Read itHow a CD Ladder Works (and When Each Rung Matures)

A plain-English walkthrough of CD ladders: staggered maturities, APYs, early-withdrawal penalties, FDIC limits, and the year-by-year math.

Read it

Money Scale Weekly

Read another one like this on Thursday?

We send one short, sourced money read per week. Tied to refinance break even and the other Money Scale pillars. Free, no spam, one click to unsubscribe.

Drop your email and you're in. We send one short read on Thursday — and nothing else without your asking.