Compound Interest, In Plain English: The Math Behind Your Future Self's Net Worth

Compound interest is the closest thing personal finance has to a cheat code. Here's the formula, the chart that makes it click, and the three numbers that matter more than picking the perfect fund.

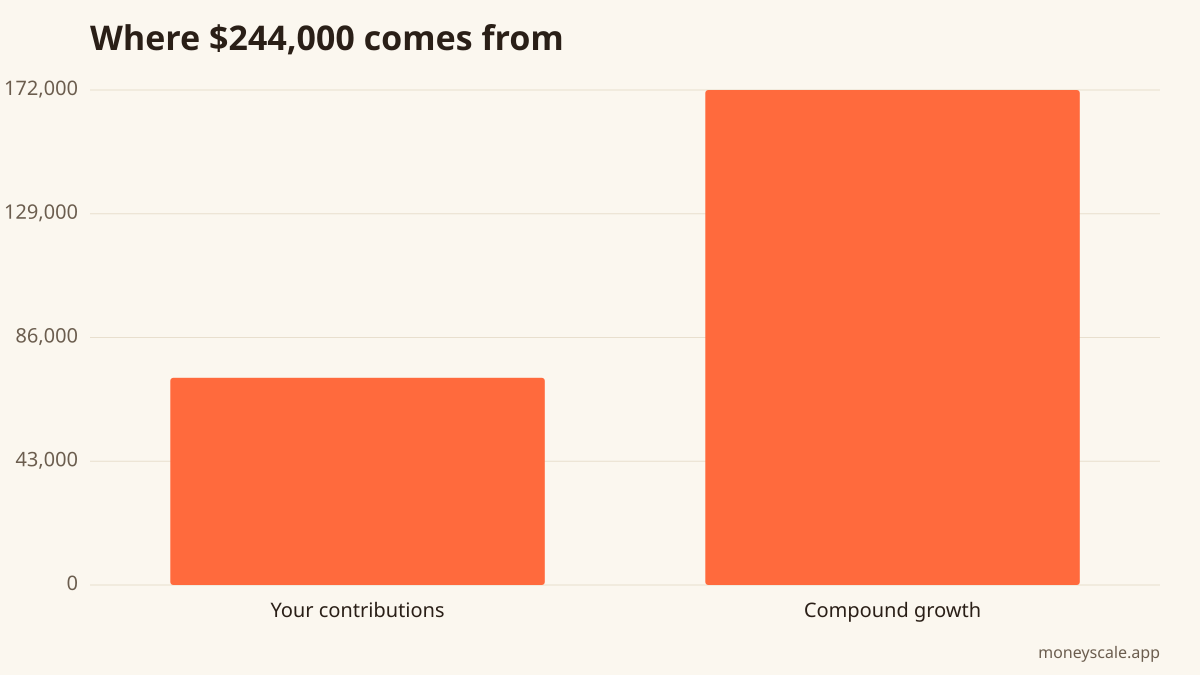

The bottom line

$200/month at 7% for 30 years = $244,000 — with only $72,000 of your money in it

If you only learn one piece of personal finance math, make it this one. Compound interest is the reason a 22-year-old who saves $200/month ends up with more money at 65 than a 32-year-old who saves $400/month — even though the 32-year-old contributes twice as much. The same math is the reason credit card debt at 24% APR feels impossible to pay off. Same engine, two directions.

Here's the formula, the chart that makes it click, and the three variables that actually matter.

The formula

Textbook compound interest is one expression:

A = P(1 + r/n)nt

- A is the amount you end up with

- P is the principal — the dollars you start with

- r is the annual interest rate, written as a decimal (7% = 0.07)

- n is how many times per year the interest compounds (12 = monthly, 4 = quarterly, 1 = annually)

- t is time in years

The exponent is the part that does the magic. Every additional year doesn't just add a constant — it multiplies what you already had by another (1 + r/n) factor. That's why the line on the chart doesn't go up in a straight line. It goes up and then it goes up.

A scenario

Put $1,000 in an account that earns 7% annually, compounded monthly. Don't add another dollar.

- After 1 year: $1,072

- After 5 years: $1,418

- After 10 years: $2,010 — your money has doubled

- After 20 years: $4,038 — it's doubled again

- After 30 years: $8,116 — it's doubled again, and you contributed nothing

That's the doubling-roughly-every-10-years pattern that drives the rule of 72: divide 72 by your annual rate (in percent) to get the approximate doubling time. At 7%, that's ~10 years. At 10%, ~7 years. At 4%, ~18 years.

Now add a monthly contribution of $200 to the same scenario. Run it for 30 years at 7%:

- You contribute $72,000 ($200 × 12 × 30)

- The final balance is roughly $244,000

- Compound growth contributed $172,000 — more than 2× what you put in

The math is in the compound interest calculator on Money Scale. Plug in your real numbers and watch the contributions-vs-growth split flip somewhere between year 15 and year 20.

The three variables that actually matter

The formula has four variables (P, r, n, t). Compounding frequency (n) is the least important — going from annual to monthly compounding at 7% over 30 years on $10,000 raises the final balance from about $76,000 to about $81,000. Real, but small.

The three that move the line dramatically are:

1. Time (t) — the cheat code

Doubling your time horizon doesn't double the result. It usually quadruples or quintuples it, because the last few doublings happen on a much bigger base.

Two savers, both contributing $200/month, both earning 7%:

- Saver A starts at 22, stops at 32. Total contributed: $24,000. Lets it grow until 65 with no further deposits. Ends with ~$355,000.

- Saver B starts at 32, contributes all the way to 65. Total contributed: $79,200. Ends with ~$326,000.

Saver A contributed less than a third of what Saver B did. They still ended with more. The only thing Saver A had that Saver B didn't was an extra ten years of compounding on the front end.

Time is the variable you can't get back. Every variable except this one can be improved later. Start now, with whatever amount doesn't hurt — even $25/month at 22 buys most of the cheat code.

2. Rate (r) — the silent killer or the silent winner

A 1% difference in annual return, compounded over 30 years on a $200/month contribution, is roughly $50,000-$80,000 of final-balance difference. One percentage point.

This is why fees matter so much. An actively-managed mutual fund charging 1% per year is, in effect, "lending" you the market's returns and keeping a percentage point of them for the fund manager's pocket. Over a 30-year career, you're handing them tens of thousands of dollars of your retirement.

Broad-market index funds charge 0.03% – 0.20%. Total stock market ETFs, S&P 500 trackers, target-date funds at major brokerages — all in this range. That's not "cheap." That's the floor. Anything dramatically above it needs a very good reason.

3. Starting amount (P) — surprisingly minor

Counterintuitively, starting with $10,000 vs. starting with $1,000 matters far less than starting at 22 vs. starting at 32, or earning 7% vs. earning 6%. The monthly contribution becomes the dominant force after the first 5-10 years.

This is good news: nobody needs to "wait until I have enough to start." A $50 starting balance with a $50/month contribution compounds nearly identically to a $5,000 starting balance with a $50/month contribution after the 20-year mark.

Compound interest going the other way

The exact same engine runs credit-card debt and high-interest loans. A $5,000 credit-card balance at 24% APR, making only the minimum payment, takes 20+ years to pay off and costs roughly $11,000 in interest — more than 2× the original balance.

It's the same formula, just running on you instead of for you. (Run it on the Money Scale debt-payoff calculator to see what your specific balance and APR cost over time.)

The avalanche method targets this: pay extra on the highest-APR debt first, because that's where compounding works against you fastest. Once that's gone, the freed-up payment rolls to the next-highest APR, and the snowball flips into something more like an avalanche.

What this means in practice

Three moves that put compound interest to work, in priority order:

- Open a Roth IRA at the earliest possible moment, even if you can only contribute $25/month. A Roth IRA at age 22 has 43 years of compounding by retirement. The number-of-years variable is doing more work than the amount-per-month variable for the first five years.

- Capture every dollar of employer 401(k) match. A 100% match on the first 6% of your salary is, mathematically, a 100% return on those contributions before market growth even starts compounding. Anything else you do is downstream of this.

- Keep total annual fund fees below 0.20% on long-horizon money. One percentage point of fees compounded over 30 years is real-money different from no-fee. The S&P 500 index fund at your broker (whichever broker you have) is almost always the right starting point.

The math you can do in 60 seconds

You don't need a calculator to estimate where you'll land. The rule of 72 divides 72 by your annual rate to get your doubling time. The rule of 114 divides 114 by your rate to get your tripling time.

At 7%, your money doubles roughly every 10 years and triples roughly every 16 years. Three doublings (about 30 years at 7%) = 8× your starting balance. Add ongoing contributions and the multiplier on what you've already saved keeps stretching that out further.

Try it: a 25-year-old with $5,000 in a Roth IRA at 7% has approximately 4 doubling cycles by age 65. $5,000 → $10,000 → $20,000 → $40,000 → $80,000, before adding a single additional dollar.

That's compound interest. The rest of investing is footnotes.

What to do this week

- Run your actual age, target retirement age, and current contribution rate through the compound interest calculator on Money Scale. The headline number will probably surprise you.

- Check your employer 401(k) match. If you're contributing less than the match cap, raise it tomorrow.

- Look up the expense ratio on every fund you own. Anything above 0.5% on a long-horizon account is worth a second look — especially if there's a cheaper index fund inside the same account that does roughly the same thing.

This is educational only and not financial advice. Real-world returns vary year to year; the historical averages cited here are illustrative and your individual outcomes will differ. For decisions specific to your situation, talk to a Certified Financial Planner or a fee-only fiduciary.

Run your numbers

Plug your own figures into the Compound Interest calculator and see your specific outcome.

Open Compound InterestSources

Related reads

How to Start Investing With $100 (a Boring, Three-Step Plan)

You don't need thousands to start investing. Fractional shares and zero-commission brokerages mean $100 is plenty. Here's the simple, evidence-based plan: one account, one diversified fund, one automatic monthly transfer.

Read itAPR vs APY: What's the Difference (With the Formula)

APR vs APY: APR is the plain annual rate, APY adds compounding. Both formulas, plus exactly how much the gap is worth at 6%.

Read itDollar-Cost Averaging (DCA): The Case for Boring, Automated Buying

Dollar-cost averaging means investing a fixed amount on a regular schedule, no matter the price. Here's why it removes timing stress, when lump-sum investing actually beats it, and why most people are already doing DCA without realizing it.

Read itIndex Funds vs ETFs: The Honest Differences That Actually Matter

Index funds and ETFs do almost the same job. Here's where the differences actually move dollars — tax treatment, trading mechanics, fees, and the case where each one wins.

Read it

Money Scale Weekly

Read another one like this on Thursday?

We send one short, sourced money read per week. Tied to investing basics and the other Money Scale pillars. Free, no spam, one click to unsubscribe.

Drop your email and you're in. We send one short read on Thursday — and nothing else without your asking.