How a CD Ladder Works (and When Each Rung Matures)

A plain-English walkthrough of CD ladders: staggered maturities, APYs, early-withdrawal penalties, FDIC limits, and the year-by-year math.

Written with AI assistance; every figure is checked against our calculators and primary sources, and reviewed by Ethan Ginsberg before publishing.

The bottom line

A $50,000 ladder split into five $10,000 CDs gives one rung—starting at $10,430 in year one—coming due every year through 2031.

A CD ladder splits one lump sum across certificates of deposit that mature in staggered years (say 1, 2, 3, 4, and 5 years), so one chunk comes due annually. As of the FOMC's June 17, 2026 decision to hold its target rate steady, CD yields sit roughly flat. Each maturing rung then reinvests into a new long-term CD.

What is a CD, and what does "APY" mean?

A certificate of deposit (CD) is a deposit account where you agree to leave money with a bank for a fixed term—the length of time, like 12 or 60 months—in exchange for a fixed interest rate. The APY (annual percentage yield) is the rate after compounding is figured in, so it tells you the true yearly return. A 12-month CD at a 4.30% APY pays $430 on a $10,000 deposit over one year.

Unlike a savings account, a standard CD rate is locked when you open it. Open a 5-year CD today, and its APY stays the same for all five years regardless of what the Federal Reserve does later. That fixed quality is the whole reason ladders exist: they lock current rates on part of your money while keeping the rest reachable sooner.

The FOMC (the Federal Reserve committee that sets the federal funds target rate) kept that rate unchanged at its June 17, 2026 meeting, per the Federal Reserve. When the policy rate holds flat rather than falling, newly issued CD APYs tend to stay roughly level too.

How do you build a CD ladder?

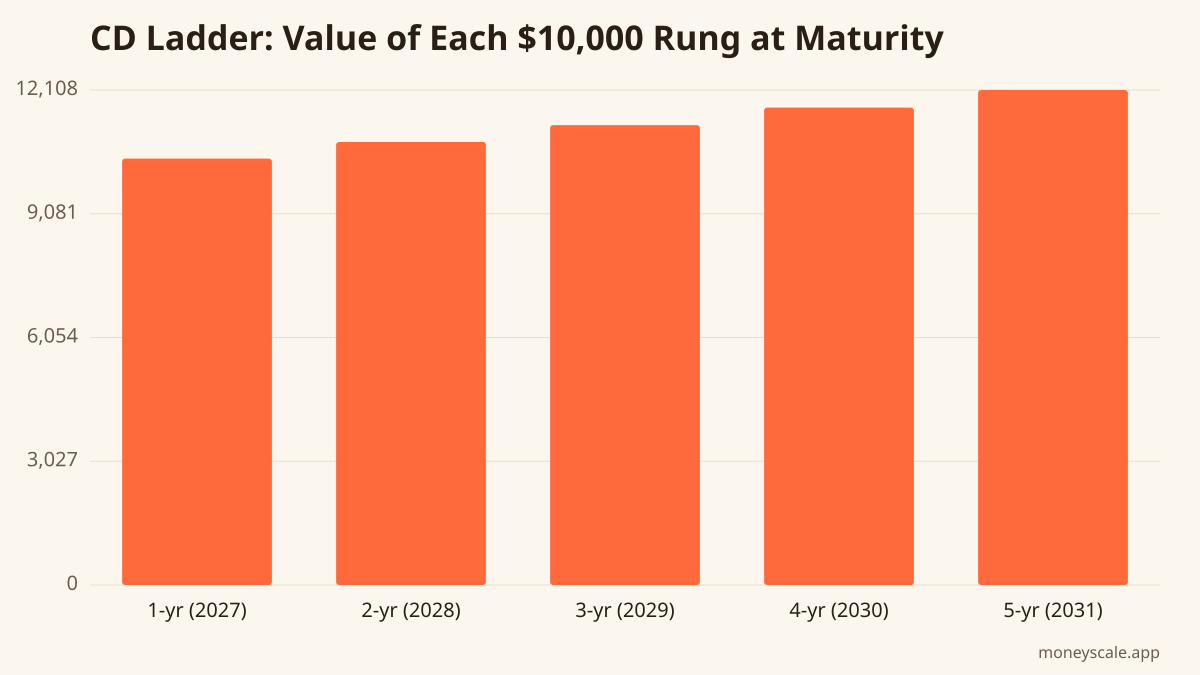

The mechanics are simple. Take a lump sum, divide it into equal pieces, and buy CDs with terms one year apart. Here's a $50,000 example split into five $10,000 rungs at sample June 2026 APYs.

| Rung | Term | APY | Deposit | Value at maturity | Matures |

|---|---|---|---|---|---|

| 1 | 1 year | 4.30% | $10,000 | $10,430.00 | Jun 2027 |

| 2 | 2 years | 4.10% | $10,000 | $10,836.81 | Jun 2028 |

| 3 | 3 years | 4.00% | $10,000 | $11,248.64 | Jun 2029 |

| 4 | 4 years | 3.95% | $10,000 | $11,677.40 | Jun 2030 |

| 5 | 5 years | 3.90% | $10,000 | $12,108.15 | Jun 2031 |

The year-one rung grows to $10,430.00, the two-year rung to $10,836.81, the three-year rung to $11,248.64, the four-year rung to $11,677.40, and the five-year rung to $12,108.15. APYs shown are illustrative; real quotes change daily.

Model your own deposit amounts, APYs, and terms rung by rung with the CD calculator.

What happens when a CD rung matures?

This is the part that makes it a "ladder" instead of a one-time purchase. When the 1-year rung comes due in June 2027, you reinvest that cash into a new 5-year CD. A year later the original 2-year rung matures, and it too rolls into a fresh 5-year CD. After five years, every rung is a 5-year CD. Because you started them in different years, one still matures every single year.

The result is a rolling cycle: long-term rates on most of your balance, plus one rung becoming available each year with no penalty for cashing it in.

How do early-withdrawal penalties work?

Pull money out of a CD before its term ends, and the bank typically charges an early-withdrawal penalty—a forfeiture of some interest. The Consumer Financial Protection Bureau notes these penalties are commonly expressed as a set number of months of interest (for example, 90 days' or 180 days' worth), and the exact amount is set in your account agreement. On shorter CDs, a penalty can sometimes eat into principal if you haven't earned enough interest yet.

A ladder is built specifically to reduce the need to break a CD. Because a rung matures every year, predictable cash needs can be met with whichever rung is coming due, instead of forcing an early withdrawal on a longer CD and eating the penalty.

How is FDIC insurance counted on a CD ladder?

The FDIC insures deposits, including CDs, up to $250,000 per depositor, per insured bank, per ownership category, according to the FDIC. "Ownership category" refers to how an account is held—single, joint, certain retirement accounts, and so on—and each category gets its own $250,000 limit at the same bank.

A $50,000 ladder at one FDIC-insured bank sits well under that cap. Larger ladders that would exceed $250,000 in one category at one bank fall outside coverage on the excess unless the deposits are spread across categories or separate insured banks.

How does a CD ladder compare to one lump-sum CD?

Putting the full $50,000 into a single 5-year CD at 3.90% would grow to $60,540.77 at maturity in 2031. That can out-earn a ladder when long rates sit above short rates, but every dollar is locked for the full five years, and reaching any of it early triggers a penalty.

The ladder trades a slice of that yield for access. Part of the balance carries shorter terms (and often slightly different APYs), and one rung frees up each year. The single CD concentrates on one rate and one date; the ladder spreads across five rates and five dates. They are different liquidity-versus-yield structures, and the CD calculator lets you compare the maturity value of each setup side by side.

Quick glossary

- CD: a fixed-term deposit account with a locked rate.

- Term: how long you agree to leave the money in.

- APY: yearly return after compounding.

- Rung: one CD within the ladder.

- Early-withdrawal penalty: interest forfeited for cashing out before the term ends.

- FDIC insurance: federal deposit coverage up to $250,000 per depositor, per bank, per ownership category.

Sources

Related reads

What Is the Fed Dot Plot? How to Read the SEP

A plain-English guide to the Fed's dot plot and the Summary of Economic Projections, with the June 17, 2026 release time and how to read the median dot.

Read itHow Travel Nurse Pay Works: Base Rate + Tax-Free Stipends

Travel nurse pay is a low taxable base hourly rate plus tax-free housing and meal stipends. Here's how the blended rate works and how to read a pay package.

Read itHow to Pay Off Credit Card Debt: The 4-Step Plan That Works on $5K or $50K

A plain-English, four-step plan to pay off credit card debt — stop the bleeding, pick a payoff order, cut the interest rate, and automate it. Works the same whether you owe $5,000 or $50,000.

Read itMid-2026 Check: Are You on Pace to Max Out Your 401(k)?

A mechanical, no-advice walkthrough of the math that tells you whether your current 401(k) deferral hits the 2026 IRS cap by December 31.

Read it

Money Scale Weekly

Read another one like this on Thursday?

We send one short, sourced money read per week. Tied to cd and the other Money Scale pillars. Free, no spam, one click to unsubscribe.

Drop your email and you're in. We send one short read on Thursday — and nothing else without your asking.