Student Loan Autopay Discount Jumps to 1% on July 1, 2026

The federal autopay interest-rate discount rises from 0.25 to a full 1 percentage point on July 1, 2026. Here's how it works, who qualifies, and what one point does to total interest.

Written with AI assistance; every figure is checked against our calculators and primary sources, and reviewed by Ethan Ginsberg before publishing.

The bottom line

The federal student loan autopay discount rises from 0.25 to 1.00 percentage point starting July 1, 2026, with a September 30, 2026 enrollment deadline.

Starting July 1, 2026, the autopay discount on federal Direct Loans rises from 0.25 to a full 1.00 percentage point, the U.S. Department of Education announced June 18, 2026. Borrowers must enroll in automatic debit by September 30, 2026 to lock it in, and the enhanced level runs through June 30, 2028.

What exactly changed on July 1?

Autopay, which the Department calls auto-debit, means your loan servicer pulls your monthly payment automatically from a bank account on the due date. Federal Direct Loan borrowers who use it have always received a 0.25 percentage point reduction on their interest rate as long as the auto-debit stays active. That benefit is documented on Federal Student Aid's auto-debit page (studentaid.gov).

The Department's June 18, 2026 announcement raises that reduction to 1.00 percentage point. Here are the key dates and figures:

| Item | Detail |

|---|---|

| Old discount | 0.25 percentage point |

| New discount | 1.00 percentage point |

| Effective date | July 1, 2026 |

| Enrollment deadline | September 30, 2026 |

| Enhanced level runs through | June 30, 2028 |

| Applies to | Federal Direct Loans |

A percentage point is an absolute change to the stated rate, not a percentage of it. A 6.39% rate minus 1.00 percentage point becomes 5.39%.

Do I have to do anything if I'm already on autopay?

No. The Department says borrowers already enrolled in auto-debit receive the additional 0.75 percentage point cut automatically. The 0.25 they already had plus 0.75 more equals the new 1.00. Borrowers not yet enrolled need to sign up through their loan servicer by September 30, 2026 to qualify.

The Department also reported a striking participation gap: only about 40% of borrowers actively repaying are currently on autopay, down from roughly 80% before the pandemic-era payment pause. A large share of repaying borrowers get no discount at all today.

Which loans qualify for the autopay discount?

The discount applies to federal Direct Loans. Some reporting has cited a narrower eligibility window tied to disbursement dates. The precise list of qualifying Direct Loans is spelled out in the Department's own materials, and borrowers can confirm their loan type and eligibility through their account on studentaid.gov rather than relying on secondhand summaries. The auto-debit benefit historically has not applied to defaulted loans or loans in certain statuses, which Federal Student Aid notes on its auto-debit page.

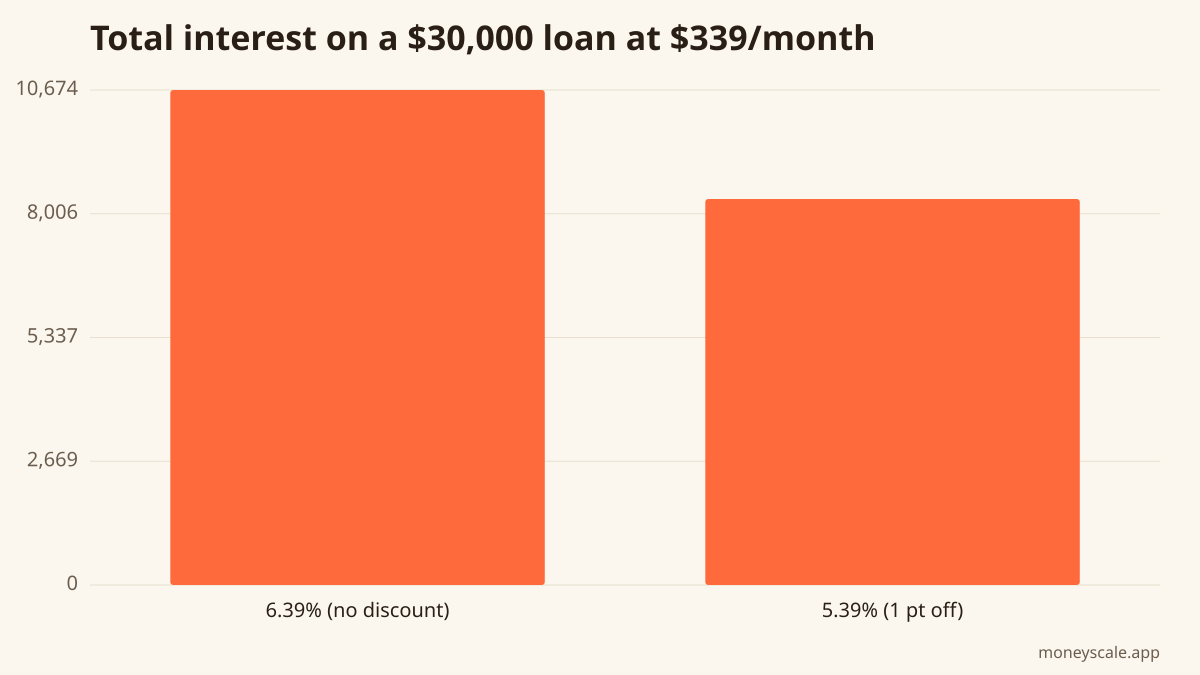

How much does one percentage point actually save?

Here's the math, using a round example. Federal Student Aid lists the 2025–2026 fixed rate for undergraduate Direct Subsidized and Unsubsidized Loans at 6.39%. Take a $30,000 balance on a standard 10-year schedule. At 6.39%, the level monthly payment is about $339.

Keep that same $339 monthly payment and compare the two rates:

| Interest rate | Total interest paid | Payoff time |

|---|---|---|

| 6.39% (no discount) | about $10,674 | ~120 months |

| 5.39% (1.00 pt off) | about $8,324 | ~113 months |

Shaving one percentage point off the rate while holding the payment steady cuts total interest by roughly $2,350 and clears the balance about seven months sooner. You can run your own balance and rate at /tools/student-loan.

One caveat: the example assumes the lower rate holds for the full repayment term, which makes the size of one percentage point easy to see. The enhanced 1.00-point reduction is scheduled to run from July 1, 2026 through June 30, 2028. The dollar effect during that window depends on your balance, rate, and payment.

Why does autopay lower the rate at all?

For the lender, automatic payments reduce missed and late payments, so the discount is a standard incentive to enroll. For the borrower, the rate cut and the convenience are the trade for letting the servicer debit the account on schedule. The benefit lasts only while auto-debit stays active; if the automatic payments stop, the reduction stops with them, per Federal Student Aid's auto-debit terms. General education on student loan servicing and automatic payments is also available from the Consumer Financial Protection Bureau (consumerfinance.gov).

What are the key dates for the 1 percent autopay discount?

Three dates matter: the change took effect July 1, 2026; the enrollment deadline to lock in the 1.00-point reduction is September 30, 2026; and the enhanced level is scheduled through June 30, 2028. Borrowers already on autopay get the extra 0.75 point automatically. Everyone else enrolls through their servicer.

Run your numbers

Plug your own figures into the Student Loan calculator and see your specific outcome.

Open Student LoanSources

Related reads

Federal Student Loan Interest Rates for 2026–27: How the July 1 Rate Is Set

The new fixed rates for federal Direct loans disbursed July 1, 2026–June 30, 2027, the Treasury-plus-add-on formula that sets them, and how one rate point changes a payment.

Read itStudent Loan Payoff Strategy: Federal vs Private, IDR vs Standard, Refi Math

Student loans aren't one debt — they're a portfolio with different rules depending on type. Here's the order to attack them, when refinancing helps (and hurts), and when forgiveness is a real plan.

Read itRent vs. Buy in 2026: How to Run the Numbers

With the Fed holding rates steady in June 2026 and its dot plot tilting away from cuts, here's the factual math behind renting versus buying — and a calculator to plug in your own numbers.

Read itHow Money Market Fund Yields Work After the June 2026 Fed Meeting

A plain-English look at what a money market fund is, how its yield tracks the federal funds rate, and why those yields stayed near current levels after the Fed held rates on June 17, 2026.

Read it

Money Scale Weekly

Read another one like this on Thursday?

We send one short, sourced money read per week. Tied to student loan and the other Money Scale pillars. Free, no spam, one click to unsubscribe.

Drop your email and you're in. We send one short read on Thursday — and nothing else without your asking.