Federal Student Loan Interest Rates for 2026–27: How the July 1 Rate Is Set

The new fixed rates for federal Direct loans disbursed July 1, 2026–June 30, 2027, the Treasury-plus-add-on formula that sets them, and how one rate point changes a payment.

Written with AI assistance; every figure is checked against our calculators and primary sources, and reviewed by Ethan Ginsberg before publishing.

The bottom line

New undergraduate Direct loans disbursed in 2026–27 carry a fixed 6.15% rate, set from the May 2026 10-year Treasury auction plus a 2.05-point statutory add-on.

Federal Direct loans first disbursed between July 1, 2026 and June 30, 2027 carry new fixed rates: 6.52% for undergraduate loans, 8.07% for graduate/professional Direct Unsubsidized loans, and 9.07% for Direct PLUS loans, per Federal Student Aid's June 4, 2026 announcement. Each rate stays fixed for the life of the loan.

What are the new federal student loan interest rates for 2026–27?

Federal Student Aid (the U.S. Department of Education office that runs federal aid) publishes the rates each year before the July 1 start of the new loan period. The figures below come from the FSA Partners electronic announcement dated June 4, 2026 and the studentaid.gov "Interest Rates for New Direct Loans" page.

| Loan type | Borrower | Fixed rate (2026–27) | Statutory cap |

|---|---|---|---|

| Direct Subsidized & Unsubsidized | Undergraduate | 6.52% | 8.25% |

| Direct Unsubsidized | Graduate/professional | 8.07% | 9.50% |

| Direct PLUS | Graduate & parents | 9.07% | 10.50% |

"Fixed" means the rate locks when the loan is disbursed and never moves, regardless of what Treasury yields or the Fed do afterward.

How is the July 1 rate actually set?

No one chooses the rate. A formula written into federal law sets it, and two pieces go into that formula.

The first piece is the high yield of the last 10-year Treasury note auction in May. A Treasury note is a loan to the federal government; its "high yield" at auction is the highest accepted interest rate bidders pay. That single number, reported by TreasuryDirect, becomes the base for every Direct loan rate that takes effect the following July 1.

The second piece is a fixed add-on, a set number of percentage points stacked on top of that Treasury yield. Each loan type gets a different add-on:

| Loan type | Add-on above 10-yr Treasury | Statutory cap |

|---|---|---|

| Undergraduate Direct | +2.05 points | 8.25% |

| Graduate Direct Unsubsidized | +3.60 points | 9.50% |

| Direct PLUS | +4.60 points | 10.50% |

So with the May 2026 10-year auction high yield at 4.468%, the undergraduate rate works out to 4.468% + 2.05% = 6.52%, the graduate rate to 4.468% + 3.60% = 8.07%, and PLUS to 4.468% + 4.60% = 9.07%. The result is then capped: even if the formula produced a higher number, the rate could not exceed the cap in the table.

Do these rates change my existing loans?

No. The 2026–27 rates attach only to new loans disbursed between July 1, 2026 and June 30, 2027. A federal Direct loan you already hold keeps the fixed rate it had when it was disbursed. Last year's loans carry last year's rate, and next year's auction will reset the rate again for loans disbursed after July 1, 2027. Each annual batch of loans is locked to its own number for the full repayment period.

Are there fees on top of the interest rate?

Yes. Federal Direct loans charge a one-time origination fee (also called a loan fee), deducted from each disbursement before the money reaches the school. Per studentaid.gov, for loans first disbursed on or after October 1, 2020, the fee is 1.057% on Direct Subsidized and Unsubsidized loans and 4.228% on Direct PLUS loans. A $10,000 PLUS loan, for example, disburses about $9,577 after the fee, even though the borrower repays the full $10,000 plus interest. The interest rate and the origination fee are separate costs.

How much does one rate point change a payment?

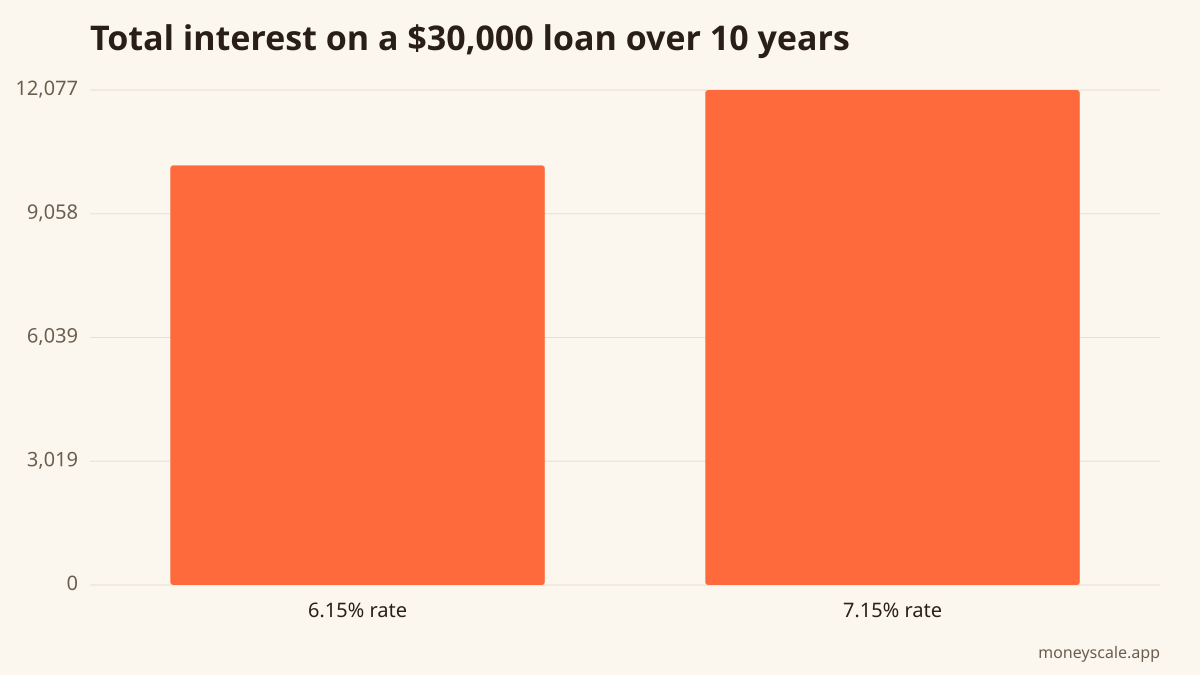

The arithmetic is the clearest way to see what a rate change does. As an illustration, take a $30,000 balance on the standard 10-year (120-month) repayment plan and compare a 6.15% rate against a 7.15% rate, one point higher.

At 6.15%, the monthly payment is about $335, and total interest over 10 years runs about $10,237. At 7.15%, the payment rises to about $351, with total interest near $12,077. That single point adds roughly $15 a month and about $1,840 in interest over the life of the loan.

The student loan calculator can show the monthly payment and total interest for other balance, rate, and term combinations.

What is the 2026–27 rate formula in one line?

The 2026–27 rate equals the May 2026 10-year Treasury auction high yield plus a statutory add-on of 2.05 points (undergrad), 3.60 points (graduate), or 4.60 points (PLUS), capped at 8.25%, 9.50%, and 10.50%. It is fixed for the life of each loan disbursed in the July 1, 2026–June 30, 2027 window, and origination fees apply on top.

Run your numbers

Plug your own figures into the Student Loan calculator and see your specific outcome.

Open Student LoanSources

Related reads

Student Loan Payoff Strategy: Federal vs Private, IDR vs Standard, Refi Math

Student loans aren't one debt — they're a portfolio with different rules depending on type. Here's the order to attack them, when refinancing helps (and hurts), and when forgiveness is a real plan.

Read itHow Money Market Fund Yields Work After the June 2026 Fed Meeting

A plain-English look at what a money market fund is, how its yield tracks the federal funds rate, and why those yields stayed near current levels after the Fed held rates on June 17, 2026.

Read itMid-Year 2026 Paycheck Checkup: Is Your Tax Withholding on Track?

How federal withholding works, why June is the natural time to check it, and how to use the free IRS Tax Withholding Estimator for 2026.

Read itMid-2026 Check: Are You on Pace to Max Out Your 401(k)?

A mechanical, no-advice walkthrough of the math that tells you whether your current 401(k) deferral hits the 2026 IRS cap by December 31.

Read it

Money Scale Weekly

Read another one like this on Thursday?

We send one short, sourced money read per week. Tied to student loan and the other Money Scale pillars. Free, no spam, one click to unsubscribe.

Drop your email and you're in. We send one short read on Thursday — and nothing else without your asking.