Mid-2026 Check: Are You on Pace to Max Out Your 401(k)?

A mechanical, no-advice walkthrough of the math that tells you whether your current 401(k) deferral hits the 2026 IRS cap by December 31.

Written with AI assistance; every figure is checked against our calculators and primary sources, and reviewed by Ethan Ginsberg before publishing.

The bottom line

The 2026 employee 401(k) deferral cap is $24,500, and at the year's midpoint the per-paycheck math is simply (limit − contributed so far) ÷ remaining paychecks.

For 2026 the IRS caps employee 401(k) deferrals at $24,500, plus an $8,000 catch-up at age 50+, or $11,250 for ages 60–63. To check your mid-year pace, subtract what you've deferred so far from your limit, then divide by the paychecks left in the year. That per-check amount lands you at the cap by December 31.

What are the 2026 401(k) contribution limits?

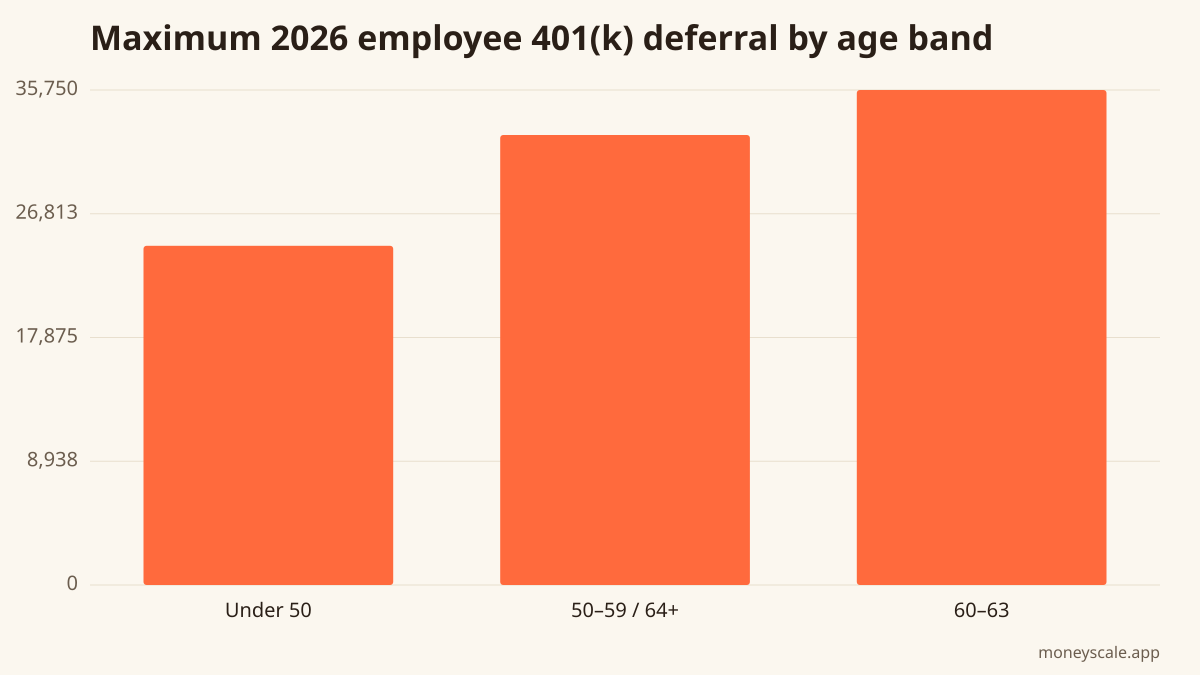

Two numbers matter here, and people mix them up constantly. The first is the employee elective deferral limit, the money you redirect from your own paycheck into the plan before tax (or after, for Roth). For 2026 the IRS set that at $24,500, up from $23,500 in 2025. The figure comes from the IRS's annual cost-of-living adjustment for retirement plans, published in November 2025 (IRS, "401(k) and profit-sharing plan contribution limits").

On top of that sits a catch-up contribution, extra room the tax code grants older savers. For 2026 it is $8,000 for anyone who reaches age 50 by year-end. SECURE 2.0, a 2022 retirement law, added a larger "super catch-up" for people who are ages 60, 61, 62, or 63 during the year: $11,250 instead of $8,000 (IRS, "Retirement topics — Catch-up contributions").

| Your age during 2026 | Base deferral limit | Catch-up | Max employee deferral |

|---|---|---|---|

| Under 50 | $24,500 | — | $24,500 |

| 50–59, or 64+ | $24,500 | $8,000 | $32,500 |

| 60–63 | $24,500 | $11,250 | $35,750 |

How do you check if you're on pace at mid-year?

The pacing formula has three inputs, all on your latest pay stub or plan portal:

- Your limit for the year (from the table above).

- Year-to-date deferrals, the total you've put in through your most recent paycheck.

- Paychecks remaining in 2026 after today.

The math:

(annual limit − contributed year-to-date) ÷ remaining paychecks = per-paycheck deferral needed to hit the cap.

If your current per-paycheck deferral sits above that number, you reach the cap before year-end. If it sits below, the current rate lands you under the limit on December 31. The formula is pure arithmetic. It describes where a given deferral rate ends up, not what rate anyone ought to pick.

Pay frequency changes "remaining paychecks." A biweekly schedule pays 26 times a year; semi-monthly pays 24; weekly pays 52; monthly pays 12. Count the pay dates left on the calendar, not the months.

What does the 401(k) pacing math look like worked out?

Take someone under 50, so the limit is $24,500. They're paid biweekly, 26 checks a year. By mid-June their plan portal shows $10,000 deferred year-to-date, and 14 paychecks remain in 2026.

Plug it in:

- $24,500 − $10,000 = $14,500 of room left.

- $14,500 ÷ 14 paychecks = $1,035.71 per paycheck to finish exactly at $24,500.

Say this saver currently defers $900 per check. Fourteen more checks add $12,600, landing them at $22,600, short of the cap by $1,900. Raising the deferral to about $1,036 per check closes the gap by December 31. The same formula works for a 60-year-old; just swap $24,500 for $35,750.

Does the employer match count toward the $24,500 limit?

No. The $24,500 (and the catch-up amounts) apply only to your own elective deferrals. Money your employer puts in, a match or a profit-sharing contribution, sits outside that ceiling. The U.S. Department of Labor describes 401(k) plans as employer-sponsored retirement plans governed by federal law (DOL, "Types of Retirement Plans").

Employer dollars count toward a separate, much larger figure the IRS calls the annual additions limit (Internal Revenue Code section 415(c)). For 2026 that combined cap on employee plus employer contributions is $72,000, not counting catch-up (IRS, "401(k) plans"). So a worker can defer the full $24,500 and still receive thousands in employer match without bumping into the personal deferral limit. The two limits are tracked independently.

Does unused 401(k) room roll into 2027?

No. The elective deferral limit is use-it-or-lose-it by calendar year. Whatever room you don't fill by December 31, 2026 does not carry forward; January 1, 2027 starts a fresh limit at whatever the IRS sets for that year. The deadline that matters for 2026 deferrals is the year's final paycheck date, which arrives before December 31 on most payroll calendars.

One more distinction: 401(k) deferrals are capped at the paycheck/plan-year level, while IRA contributions for a tax year can generally be made up to the filing deadline the following spring. The 401(k) clock does not extend into the next year.

How can you model the remaining-paycheck amount?

If you'd rather skip the division by hand, the 401(k) calculator takes your limit, year-to-date total, and remaining paychecks and returns the per-check figure. It also shows how the employer match stacks separately on top of your own deferrals. The SEC's investor education site explains how 401(k) plans work for savers who want the background (Investor.gov, "401(k) Plan"). The output is descriptive math: where a chosen deferral rate lands by year-end, using the 2026 IRS limits above.

The figures here reflect the 2026 limits the IRS published in its November 2025 cost-of-living adjustment. Confirm your own year-to-date number and pay schedule against your plan statement before running the formula.

Run your numbers

Plug your own figures into the 401(k) Projection calculator and see your specific outcome.

Open 401(k) ProjectionSources

Related reads

How to Read the CPI Report: What May 2026 Means for Your Dollar

A plain-English guide to the Consumer Price Index, how the BLS builds headline and core CPI, and what the May 2026 release says.

Read itQ2 Estimated Taxes Are Due June 15, 2026: How Quarterly Payments Work

The second-quarter 2026 federal estimated tax payment is due June 15. Here is how quarterly payments work, who owes them, the safe-harbor rule, and how self-employment tax is figured — with the real numbers.

Read itAccredited Investor Rules (2026): Who Can Buy Private Companies

The 'accredited investor' rule is the legal gate that decides who can buy into private companies like SpaceX, OpenAI, and Anthropic. Here are the exact income and net-worth thresholds, the credential exceptions, and why the rule exists.

Read itCan You Buy SpaceX Stock? What 'Pre-IPO' Really Means (2026)

For years you could not buy SpaceX stock at all — it was a private company. In 2026 that changed when SpaceX filed to go public. Here's the honest, up-to-date picture: what 'pre-IPO' meant, how employee share sales worked, and what its IPO filing actually says.

Read it

Money Scale Weekly

Read another one like this on Thursday?

We send one short, sourced money read per week. Tied to 401k and the other Money Scale pillars. Free, no spam, one click to unsubscribe.

Drop your email and you're in. We send one short read on Thursday — and nothing else without your asking.